GOLD PRICES steadied around last Friday’s 23-week closing low in London on Wednesday, trading at $1227 per ounce as European stock markets fell and rumors spread that the Modi Government in world No.2 gold consumer India may formally ban imports of the metal amid the financial chaos caused by last week’s demonetisation of the country’s largest banknotes.

Government bonds continued their slump following Donald Trump’s victory in the US presidential election, driving longer-dated Western bond yields up near fresh 2016 highs amid news of the strongest US factory-gate inflation in 2 years.

The Dollar rose to its highest since 4 January against the single currency Euro on the FX market. The US currency’s strength likely signals a retreat of “risk appetite” according to Bank for International Settlements’ head of research, Hyun Song Shin.

But “fixed income [just] had its worst week since the ‘taper tantrum’ of mid-2013,” says precious metals analyst Jonathan Butler at Japanese conglomerate Mitsubishi Corp, “with yields on longer-dated US Treasuries exploding upwards as investors rotate out of the relative safety of US government securities and towards risk assets [such as equities].

“This has increased the cost of carry for non-yielding assets such as precious metals and made the real-rate environment (inflation-adjusted yields) less positive.”

“Yields on 10-year Treasuries went up,” agrees German bank LBBW analyst Thorsten Proettel.

“[That] is poison for gold, as a non-interest bearing asset.”

The giant SPDR Gold Trust (NYSEArca:GLD) shed another half-tonne of metal on Tuesday, as liquidation by stockholders cut the bullion needed to back its shares down to a new 5-month low below 928 tonnes.

That extended the GLD’s worst run of outflows since April 2013‘s gold price crash.

Globally, more investment fund managers now expect an upturn in consumer-price inflation than any time since 2004 according to the latest survey from Bank of America Merrill Lynch.

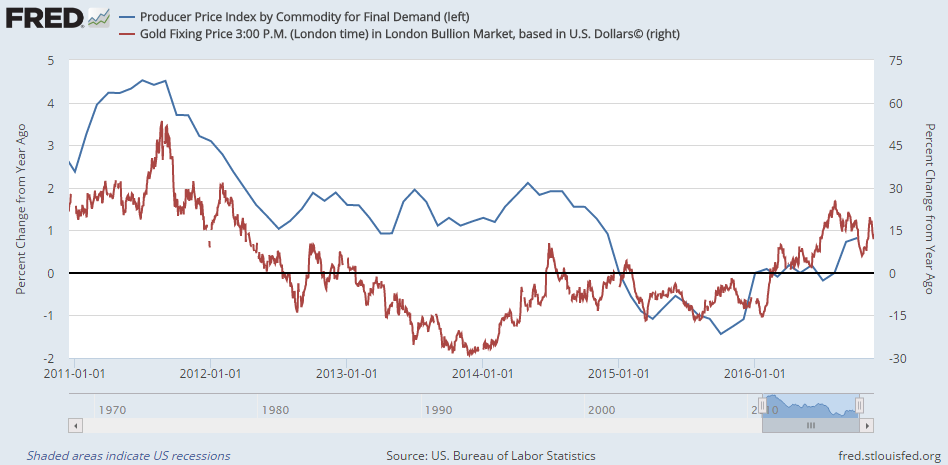

After Tuesday’s news that UK consumer-price inflation slowed to 0.9% per year in October – despite the continued slump in the Pound – today saw US producer-prices inflation miss analyst forecasts but reach a 2-year high at 0.8%.

“BAML’s survey found fears of a ‘stagflationary bond crash’ was the biggest tail-risk identified by investors,” reports the Financial Times, “at 23% – a four-year high.”

Gold importers in India meantime – the world’s second-heaviest consumer market – are placing heavy orders in fear of an outright ban on new shipments by the Modi Government, Reuters claims, highlighting rumors first reported by the Economic Times at the weekend.

“We hear from certain circles of this possibility…though nothing official is out yet,” ET quoted the pro-Modi IBJA jewelers’ association secretary Surendra Mehta on Sunday.

“The association is supportive of the government’s fight against black money…We have asked our members to support the government wholeheartedly.”

Reporting from Zaveri Bazaar in Mumbai and Karol Bagh in New Delhi, “There are ready buyers of the metal willing to pay in the old [and now illegal] bills,” says Reuters, quoting a price for cash payments in the now banned Rs500 and Rs1,000 notes of 45,000 Rupees per 10 grams – some “53% higher than the official price.”

The Times of India quotes prices as high as Rs49,000 per 10 grams for banned banknote deals in Mumbai, with no receipt.

But India’s gold and jewelry shops are apparently shut, says the Press Trust of India, as “the Income Tax Department carrie[s] out surveys following reports of alleged profiteering and efforts at tax evasion” amid the banknote demonetisation.

Comparing sales on 7 November against the 3 days following Prime Minister Narendra Modi’s move to hurt forgers and tax evaders by banning the high value banknotes, “[We] found that [gold] sales increased up to 290%,” The Times of India quotes one un-named official.

“Our Delhi headquarters will analyze data of [these] suspicious gold sales from across the country and after that action will be decided.”

“Stringent action will be initiated at the right time,” a tax official tells The Times‘ News Network

“Jewelry business has been completely paralysed across the country,” says Bachhraj Bamalwa, director of the All India Gems & Jewellery Trade Federation.

India’s gold and jewelry sector directly employs between 3 and 4 million people according to a panel discussion of senior executives at this year’s London Bullion Market Association conference.

“Demand from rural India has been hit because of less supply of cash due to the demonetisation move,” Bamalwa tells the Economic Times today.

“The market is not likely to see much buying from January to March 2017,” adds Kotak Mahindra Bank’s head of precious metals Shekhar Bhandari, “[not] until there is a clearer picture on GST on gold” – meaning the General Sales Tax rates now being discussed and set by government, with a possible 18% tax added to jewelry.