GOLD PRICES began August dead-flat from last week’s finish against a falling US Dollar on Wednesday in London, while world stock markets slipped before the latest interest-rate decision and statement from the Federal Reserve.

China’s main indices led the drop in global equity prices, losing 2% for the day as Beijing said it won’t respond to the “blackmail” of US President Trump’s new threat of higher import tariffs on Chinese goods.

Ahead of today’s Fed announcement – expected to leave rates unchanged but repeat the central bank’s plan for two more hikes in 2018 – new data from the private-sector ADP Payrolls service showed strong growth in non-farm US jobs during July.

“The job market is booming,” says economist Mark Zandi of Moody’s Analytics impacted by the deficit-financed tax cuts and increases in government spending.

“Tariffs have yet to materially impact jobs, but the multinational companies shed jobs last month, signaling the threat.”

“The trade skirmishes evolved into tariff wars and now we are possibly at the beginning of currency wars,” said Reserve Bank of India Governor Urjit Patel today, hiking interest rates for the world’s most populous nation for the second month running to try and strengthen the currency and reduce inflation.

Gold priced in Japanese Yen today held near 2-week highs after the Bank of Japan maintained its “ultra-easy” monetary policy on Tuesday.

Gold prices today rebounded €10 per ounce for Eurozone investors from yesterday’s drop to a 30-month low of €1036.

But the UK gold price in Pounds per ounce slipped once again below £930 as Sterling edged higher before Thursday’s rate decision from the Bank of England – widely expected to deliver only the second rate rise of the last decade to a level of 0.75%.

“The big institutions are pretty darn negative on the yellow metal,” said fund manager and celebrity US pundit Jim Cramer on CNBC overnight, “and I think perhaps too negative, which could be tinder for a big rally.”

Looking at non-commercial positioning in Comex gold futures derivatives, “The last time the numbers [of bullish over bearish bets] got this low was December of 2015,” Cramer says.

“How’d we do if we went long at that moment when not that many people liked it? Boom!”

“It’s always darkest before the dawn,” agrees a column on Bloomberg, “and extremely bearish positioning often heralds a turn north.

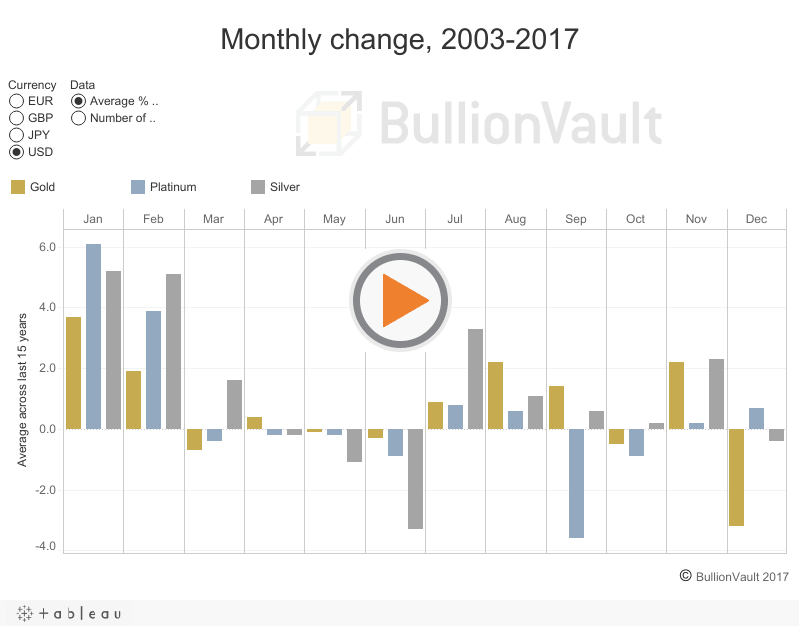

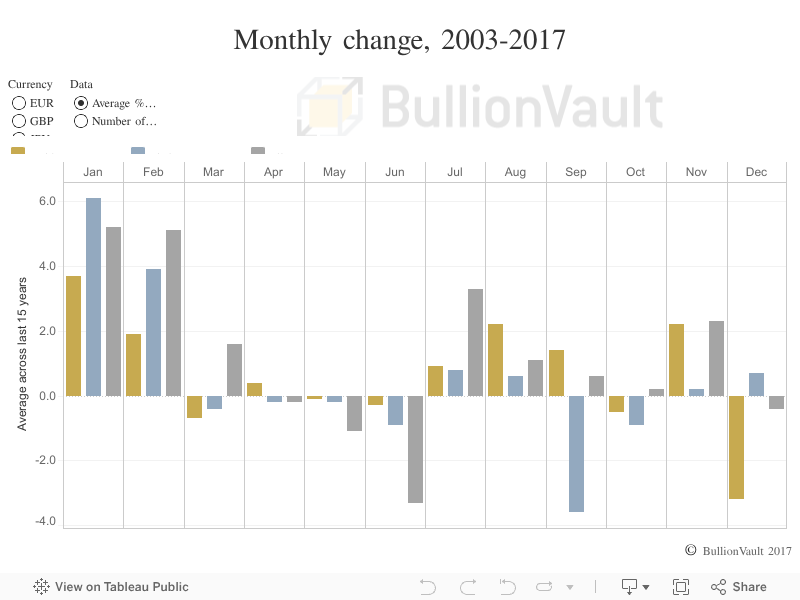

“It’s worth looking at the calendar, too. After January, August is arguably the most consistently bullish month for gold.”

Shanghai’s benchmark gold price fixed at ¥268 per gram on Wednesday, unchanged in Yuan terms from the start of both July and June but recovering to a premium over London quotes of $4.80m – around half the typical incentive for new bullion imports into the world’s No.1 gold consumer nation.

So far this week Japan’s latest industrial output data showed a surprise slowdown, China’s manufacturing PMI came in weaker than expected, the Eurozone’s economic growth missed forecasts but inflation rose to a 5-year high at 2.1%, and UK consumer confidence worsened on the Gfk survey as credit-card spending accelerated near February’s 12-year record of 9.6% annual growth.

US data has been firmer, with the number of home sales pending in June showing only a 2.5% year-on-year drop against -6.0% forecast, while ‘core’ living costs held 2.2% annual inflation on the Fed’s preferred PCE measure.

US worker compensation rose 2.8%, the fastest annual growth since summer 2008 – immediately before the Lehman’s crash and global economic slump.

“Worker pay rate hits highest level since 2008” https://t.co/pMDxHQqcg9

— Donald J. Trump (@realDonaldTrump) July 31, 2018

The Bank of England “should” raise UK interest rates as the City expects tomorrow, says the private-sector NIESR forecaster.

But “it is entirely possible that in three months time the August rate increase could look like a mistake” the think tank adds, thanks to poor Brexit negotiations or a worsening global trade war.

“The big picture of a trade war and protectionism is that it is a slow death,” says Canadian brokerage TD Securities’ global strategist Richard Kelly, “instead of anything sudden and shocking.”