EURO GOLD prices jumped to 11-month highs as London and New York re-opened after the long holiday weekend on Tuesday, breaking above €1130 per ounce as Italy’s political mess saw Rome’s short-term borrowing costs jump to the highest since the peak of the Eurozone debt crisis in 2012.

Giuseppe Conte, the chosen prime minister of Italy’s new Eurosceptic coalition of right- and left-wing parties the League and M5S, yesterday quit trying to form a government.

That left President Sergio Mattarella to nominate Carlo Cottarelli, a former official at the IMF, thereby “sidelining” the new coalition and its plans to issue a parallel currency, and probably provoking another election after the summer.

Global stock markets fell hard as the single currency Euro sank to its lowest US Dollar exchange rate since last July, dropping over 8% from February’s 3-year peak.

The price of 2-year Italian debt has halved since the end of last week, driving the yield offered to new buyers – and the rate at which Rome could borrow for that length of time today – up to 2.4% per annum.

Italy’s 2-year yields began last week below 0.17%.

Spain’s 2-year bonds also sank in price today, driving their yield back above 0% for the first time since the UK’s shock Brexit referendum in mid-2016, as Prime Minister Mariano Rajoy was told to face a vote of confidence this coming Friday over a scandal which last week saw 29 senior members of his right-wing People’s Party convicted over corruption and false accounting.

“The governance of Spain cannot be left in the hands of a political leader who has lost all credibility,” says an editorial in El Pais.

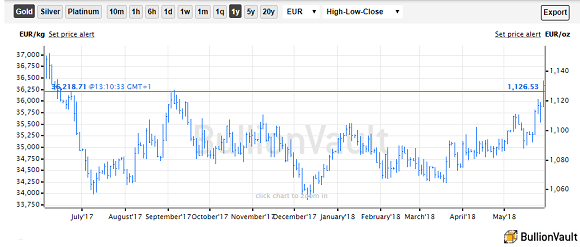

Gold priced in the Euro this morning leapt to €1133 per ounce, its highest since June 2017, before edging back to €1126.

Dollar gold prices were meantime unchanged from the weekend at $1302.

“Italy knows the rules. They might want to read them again,” said Vitor Constancio, outgoing vice-president of the European Central Bank, when asked by Germany’s Spiegel magazine if Frankfurt would rescue Italy from insolvency.

“Italy’s destiny is that of Europe,” said Ignazio Visco, governor of the Banca d’Italia, which in 2009 rebuked a move by then-prime minister Silvio Berlusconi targeting Italy’s gold bullion reserves to help pay down the country’s debt.

“There are no solutions outside the European Union…[and] there are no explanations, other than emotional, for what is happening today on the markets.”

Italy’s 2-year bond yield “is set for its biggest one-day jump in 26 years,” says the BBC.

1992 saw Italy first devalue the Lira and then quit the single Euro currency’s precursor, the Exchange Rate Mechanism, as foreign investors sold Italian assets over what one history calls “policies designed to placate the [1970s and ’80s’] social unrest with inflation and with money taken from future generations.”

Italy’s public debt then had an average time to maturity of barely 3 years against an average 7 years today, according to an infograhic from the Dipartimento del Tesoro.

An auction of new 6-month Treasury bills today achieved an average yield for investors of 1.21% per annum, the first above-zero yield for such short-term debt since September 2015 according to Il Sole 24 Ore.

A sale of 6-month bills in late April achieved an average yield of minus 0.42%.

The gap between Italian and German bond yields widened still further as the price of Berlin’s debt rose in what headline writers called a “rush to safe havens”, with the spread of 10-year BTPs over Bunds jumping Tuesday to 3.2 percentage points, the widest since March 2013.