GOLD PRICES slipped $5 per ounce from 3-week highs in London trade Wednesday morning, but held a 0.4% gain for the week so far at $1271 as world stock markets extended Wall Street’s late losses and the US Dollar continued to rise.

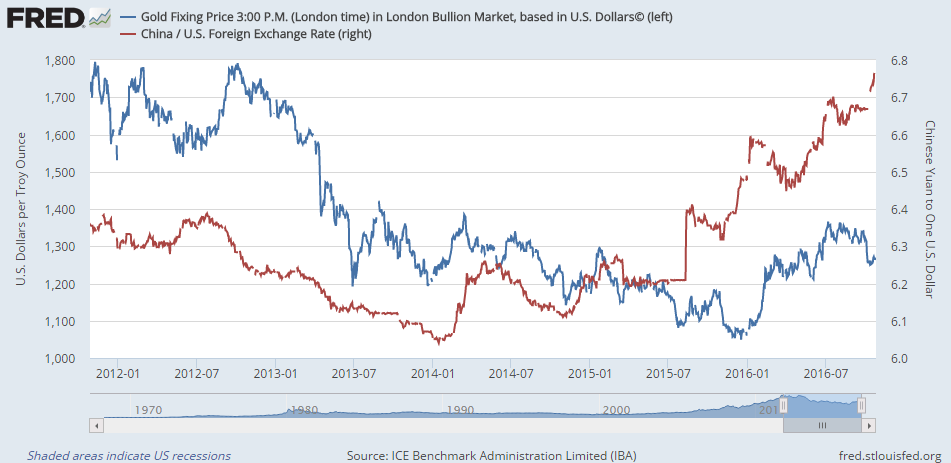

The Dollar touched fresh 6-year highs versus the Chinese Yuan, but Shanghai gold prices rose faster, holding the premium for bullion landed in the world’s No.1 consumer country at $5 per ounce above quotes for London settlement.

One day after China’s top central banker Yi Gang wrote an editorial in Beijing’s People’s Daily warning “speculators” to stop selling the Yuan, the State Administration of Foreign Exchange has imposed exchange controls to block capital outflows, says the Nikkei Asian Review, capping how much foreign currency banks in key economic regions led by Shanghai and Guangzhou can trade with customers.

“These limits, though ostensibly up to banks’ discretion, are set by negotiation with authorities and so are essentially directed by the government,” the Nikkei says, quoting a ‘source’.

“A gag order has been imposed surrounding the measures, the source said.”

“The Chinese currency has stayed stable against a basket of currencies,” said People’s Bank chief Yi in his article after the Yuan dropped 1.5% versus the Dollar over the last two weeks, “and its volatility was far below other emerging market currencies.”

British Pound gold prices meantime retreated £10 on Wednesday morning from an overnight spike to £1050 per ounce – the highest since early July’s 3-year post-EU referendum peak – as Sterling whipped on the FX market amid questions to new prime minister Theresa May over her government’s supposed “hard Brexit” strategy.

News-wire reports today attribute the rising gold price to growing Indian demand ahead of next week’s Hindu festival of Diwali.

“The metal [has seen] solid physical interest toward $1260,” says a trading desk note from Swiss refining and finance group MKS Pamp.

“To put things into perspective, Friday’s ETF outflow was the largest daily decline since mid-2013 [but] when coupled with the Greenback’s eight-month high [that] shows a high level of resilience within the gold market.”

“Gold is staging [an] expected rebound,” says a technical analysis from French investment bank and bullion market maker Societe Generale.

Gold prices “closed [Tuesday] above the 200-day [moving average], at $1273,” says a technical analysis from Scotiabank, the bullion market maker.

“New resistance comes in at $1284…Support is at $1267.80 [per ounce].”